AFFORDABLE CARE ACT (ACA/OBAMACARE)

Affordable Insurance for Individuals and Families

The Affordable Care Act (also known as Obamacare) was enacted to make health insurance coverage both guaranteed issue and affordable for more Americans. Clients who come to us for help enrolling in an ACA plan tell us their efforts to enroll themselves were baffling and frustrating and that it was easy to make a mistake. It’s our job to make enrollment simple while ensuring they are getting the best coverage for their needs. We can do the same for you whether you need coverage for an individual or family.

Your first questions might be about your coverages and costs and perhaps which doctors or hospitals you can utilize. We’ll answer your questions, ask you about your needs, and help you understand your choices and the benefits that come with them.

The ACA Provides Individuals and Families with Federal Subsidies and Tax Credits

One of the key benefits of the ACA is the availability of subsidies and tax credits that make medical insurance affordable for more people. This financial aid is based on your household income and the size of your family. Understanding these subsidies can significantly reduce your monthly premiums, making quality health insurance accessible.

At MBhealth, We Work for You, Not Insurance Companies

Our enrollment revolves around you. When we determine together which insurance plan is the best choice and with whomever the carrier turns out to be, it’s as if we are enrolling ourselves in the same product based on your specific situation. We’re here to make your enrollment simple and give you the confidence that you have the very best plan for you.

Obtaining the Right Insurance Under the ACA Can Be Challenging

We know how bewildering it is to try to navigate websites offered by the government or private insurance companies. We know just what to ask to find an individual’s best plan. We also understand situations like pre-existing conditions, divorce, assets, future retirement or COBRA coverage from prior employment.

It’s important to us to take the time to answer clients’ questions, so they have certainty that they’re getting the right plan. Some people want to see their current doctors, for example, and we can help them get a plan that enables them to do so. We will also help you fit your insurance coverage into your overall financial situation.

Understanding the Essential Health Benefits Mandated by the ACA

The ACA mandates that all health insurance plans offered through the marketplace cover a set of essential health benefits. These benefits include services like emergency care, hospitalization, maternity and newborn care, mental health services, prescription drugs, and preventive services such as screenings and immunizations. These mandates ensure that every plan will cover comprehensive care, giving you the peace of mind that your health insurance can meet your basic needs.

Do you need help understanding the benefits available to you under the ACA? Call MBhealth for assistance in finding the best plan for you and your family.

How to Obtain the Best Coverage for Your Entire Family

Whether you’re thinking of starting a family or already have one, we can help you get the best coverage for your situation. We understand how to deal with pre-existing conditions, how to help you see doctors who are important to you, how to get you the best price and so much more.

There can be complicating factors related to family health insurance, such as blended families, assets or upcoming retirement. Instead of spending hours trying to navigate a confusing website that does not ask all the right questions, call us.

Special Enrollment Periods and Qualifying Events You Should Know About

In addition to the Annual Open Enrollment Period, the ACA provides for Special Enrollment Periods (SEP) triggered by qualifying life events such as marriage, divorce, the birth of a child, or loss of other health coverage. If you experience any of these events, you may be eligible to enroll in a new plan or make changes to your existing coverage outside of the Open Enrollment Period. Understanding these provisions can help you maintain continuous coverage and avoid unnecessary stress during these life changes.

MBhealth can help Individuals with Self-Employed Health Insurance Options

If you’re self-employed, we can help you find the best health insurance for your situation. There are many options available, and we hear from people trying to navigate this maze of self-employed health insurance choices that it’s too time-consuming. Let us help you so you can focus on what’s important: growing your business.

If there are any complexities to your situation such as pre-existing health conditions, assets or COBRA coverage, we’ll walk you through the process so you can make the best choice.

What Our Clients Say

AFFORDABLE CARE ACT Frequently Asked Questions

Health insurance under the Affordable Care Act (also called Obamacare) could be free for those meeting the minimum income requirement, but this is different for each person’s situation. The person is eligible for a subsidy from the federal government that can reduce their health insurance premium to zero.

To be eligible, a person must be a U.S. citizen and live in the U.S., or be lawfully present in the country.

A person can obtain Obamacare by visiting the government website or calling them directly but with all the variables, networks, plans, and rules. It can help to have an insurance expert to consult. That’s the best way to know if you have the right plan. If you need help with Obamacare, call MBhealth.

Before making your choice of health insurance chosen from the Marketplace, it’s important to know the basic varieties of plans. Here are your some of choices:

- There are Health Maintenance Organizations where you are required to get referrals to care from doctors contracted with that HMO. You generally don’t have out-of-network care available in most situations as well.

- An Exclusive Provider Organization is one in which there is no out of network coverage available except in a life threatening emergency.

- A Preferred Provider Organization lets you use providers in and out of network without a referral.

The right choice for you will depend on where you live and the networks and plans available in your state, and the kinds of providers you expect to need in the future. Making the right decision can be challenging. MBhealth can help you make the right decision the first time. Call us for help.

The 9.5 rule relates to a determination of whether or not employer-provided health insurance coverage is considered affordable for an employee. If coverage is deemed not affordable, that person may be able to receive a subsidy from the federal government for their health insurance by obtaining it from the Marketplace.

Prior to 2022, an employer-provided health plan was deemed unaffordable if it cost an employee more than 9.5% of their income. That person could then go to the Marketplace for health insurance and get a subsidy to bring down their cost.

In 2023, what was “affordable” was redefined. The rule was revised to take into account the cost to provide health insurance for the entire family of the insured person.

This now may allow a spouse, children or both to access the tax credits/subsidies to lower the overall healthcare costs. This can be very complicated to please call MBhealth for assistance in your decision.

Anyone can qualify for health insurance under the Affordable Care Act (Obamacare). The tax credit (subsidy) you receive depends on your income, and the final premium can vary depending on your income and tax credit.

The income levels qualifying a person to receive a subsidy change slightly each year. A person with an income at or near the federal poverty level would receive a subsidy sufficient to make their health insurance potentially zero premium.

The income that should be taken into account is the income of the year in which coverage will be effective. So accurately estimating their income for the year when choosing a health insurance plan during Open Enrollment is vital. If you estimate the income too low, you could end up owing back some of the subsidy at tax time.

To work out all these details right the first time, contact MBhealth—we can help you understand the process step by step.

Your out-of-pocket limit or maximum is the most you will have to pay for covered services in a calendar year. After your expenses for deductibles, copayments and coinsurance within your network reach this figure (which changes slightly every year), your health plan covers 100% of any further covered costs as long as you stay in network.

The out-of-pocket figure does not include your monthly premiums or services not covered by your plan (such as elective or cosmetic procedures). If you go out of your network for care, these figures also cannot be included in your out-of-pocket calculations. Only the allowed or contracted rate after all discounts is counted toward your out of pocket limit.

For policies obtained on the Marketplace, the 2024 out-of-pocket limit for an individual is $9,450 and for a family is $18,900. Each year, deductibles must once again be met and your costs once again must add up to the current year’s out-of-pocket sum before the plan will cover 100% of costs in network.

The Affordable Care Act enacted in 2010 had two main purposes. One was to enable more Americans to obtain health insurance.

This main feature eliminated the problems people with pre-existing medical conditions had maintaining or affording health insurance coverage. Since most health insurance companies would not cover costs for pre-existing conditions, many people were locked into jobs that provided them with insurance. The ACA removed the worry for people with pre-existing conditions so these individuals can now make life changes and maintain insurance coverage.

Secondly, it takes into consideration each individual or family’s income situation. By doing so it allows premiums to be reduced to a more affordable level. Your income also can adjust your deductibles and out of pocket limits.

To get the best out of the ACA for yourself and your family, let MBhealth advise you on your specific situations.

Yes, anyone who has obtained health insurance from the Marketplace can make changes, renew or cancel policies during Open Enrollment periods. Open Enrollment starts November 1 and ends January 15. This is when you can renew your current plan if it still meets your needs, or change to a new one.

During this time period, you should create a new estimate of your income for the upcoming year. This figure will help determine whether or not you can receive a subsidy (premium tax credit) or benefit reduction on your health insurance.

If you take no action by December 15, you may automatically be re-enrolled in your same plan (as long as it continues to be available) with an effective date of January 1. However, a subsidy from the federal government will be based on your prior year income. It could benefit you to revisit this each year.

There are situations that enable you to enroll in plans other times throughout the year. For example, if you lose your employer health insurance because of a change in employment, you get married, divorced, or have a baby. To avoid losing any benefits due to you, let MBhealth guide your health insurance decisions!

Because of changes made by the Affordable Care Act in 2010, insurance companies can no longer charge more or refuse to provide health insurance to a person with a pre-existing condition. Pre-existing conditions could include asthma, cancer and diabetes.

Before this Act took effect, many people had to get coverage through jobs that provided them and their family health insurance. If someone developed a medical condition that would require extensive future medical care, there was no way that family could ever get an individual health insurance policy. Now, individuals can have changes in their life without worrying about losing or not having access to health insurance.

Additionally, once a person is enrolled in an Obamacare/ACA plan, the company providing coverage may not deny them coverage or raise their rates based solely on that person’s health. The same rule applies to pregnant women; once they are enrolled, their pregnancy and childbirth costs must be covered as of the effective date of the policy.

To learn about exceptions to these rules and ensure your family is fully covered, let MBhealth guide you as you make the right choices on health insurance.

There are some criteria for who can benefit from the Affordable Care Act.

- You must be an American citizen by either birth or naturalization, or be a legal non-citizen resident.

- You cannot be incarcerated, however, you can enroll in an ACA health insurance plan after being released.

- You must not be covered by Medicare. If you do have Medicare now, you cannot add a Marketplace/ACA policy to your coverage.

- Medicaid can also cause you to be ineligible as well.

Each individual or family will have their own set of circumstances that affect the coverage available. Let MBhealth work hand in hand with you during your decision.

Contact MBhealth Today for Help Making Your Best Decisions

For individual, family or self-employed health insurance, we’re the insurance agent you can trust. We serve more than 10 states, including Missouri and Illinois. Call (314) 544-5400 for a consultation or to get your questions answered. Or fill in the form below and we’ll be in touch soon.

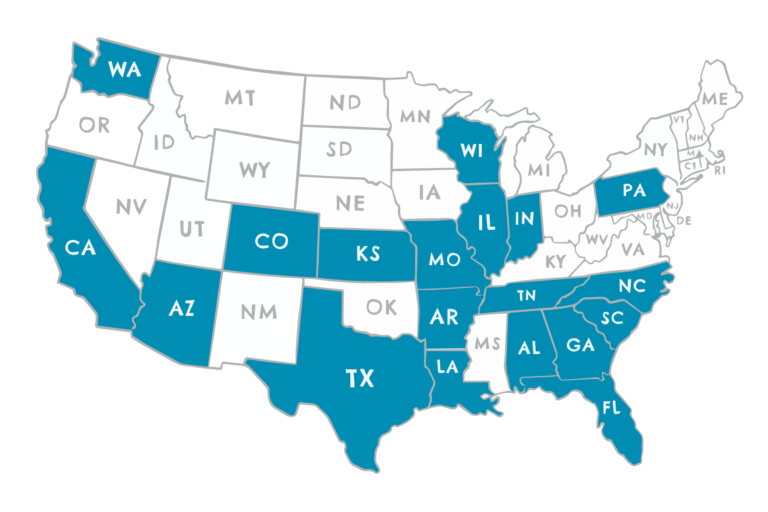

STATE LICENSURE

MBhealth is licensed in the following states:

- Alabama

- Arizona

- Arkansas

- California

- Colorado

- Florida

- Georgia

- Illinois

- Indiana

- Kansas

- Louisiana

- Missouri

- North Carolina

- Pennsylvania

- South Carolina

- Tennessee

- Texas

- Washington

- Wisconsin